23 September 2010.

Renewed economic uncertainty is testing Americans’ generation-long love affair with the stock market.

Investors withdrew a staggering $33.12 million from domestic stock market mutual funds in the first 7 months of this year,

according towards the Investment Company Institute, the actual mutual fund industry industry group.

Now many are choosing investments they deem safer, such as bonds.

If that pace continues, more money will be pulled out of those mutual funds in 2010 compared to any year since the Eighties,

with the exception of 2008, when the global financial crisis peaked.

Small traders are “losing their urge for food for risk,”

a Credit Suisse analyst, Doug Cliggott, said in a recent are accountable to investors.

One of the phenomena of the last several decades has been an upswing of the individual investor.

As Americans have become more responsible for their own pension,

they have poured money into stocks with such faith which

half of the country’s households right now own shares directly or even through mutual funds,

which tend to be by far the most popular way Americans invest in stocks.

So the turnabout is actually striking.

So is the timing.

After past recessions, ordinary investors have typically regained their enthusiasm for stocks,

hoping to profit as the economy recovered.

This time, even as company earnings have improved,

Americans have grown to be more guarded with their opportunities.

“At this stage in the economic cycle, $10 to $20 billion would usually be flowing into household equity funds”

rather than the billions that are flowing out,

said Brian Nited kingdom. Reid, chief economist of the investment start.

He added, “This is very unusual.”

The idea that stocks tend to be safe and profitable investments with time seems to have been dented

in exactly the same that a decline in home ideals and in job stability recent years

has altered Americans’ sense of financial security.

It may take many years before it is obvious whether this becomes a long-term transfer of psychology.

After technology and dot-com gives crashed in the early 2000s, for example,

investors were quick to re-enter the stock market.

Yet larger economic calamities like the Excellent Depression affected people’s behaviour toward money for decades.

For right now, though, mixed economic data is presenting a picture of

an economy that’s recovering feebly from recession.

“For several ordinary people, the economic recuperation does not feel real,”

said Loren Sibel, a senior analyst at Strategic Insight, a New York research and data firm.

“Individuals are not going to rush towards the stock market on a sustained basis

until they feel more confident of work growth

and the sustainability of the economic recovery.”

One investor who has restructured his portfolio is Gary Olsen, 51, from Dallas, tx.

Over the past four years, he has adjusted the proportion of their investments from 65 percent stocks and 35 percent bonds

so that the $1.A million he has invested is now equally balanced.

He had worked like a portfolio liquidity manager for that local Federal Home Loan Bank and retired four years ago.

“Like everyone, I lost” throughout the recent market declines, he explained.

“I needed to have a more conservative allocation.”

To be sure, a lot of money continues to be flowing into the stock market

from little investors, pension funds along with other big institutional investors.

But ordinary traders are reallocating their 401(k) retirement plans,

according to Hewitt Associates, a consulting firm that monitors pension plans.

Until two years back, 70 percent of the money in 401(nited kingdom) accounts it tracks was invested in stock funds;

that proportion fell to 49 percent by the start of 2009

as people rebalanced their portfolios toward bond investments

following the financial crisis in the drop of 2008.

It is now back again at 57 percent, but almost all of that can be attributed to the rising price of stocks in recent years.

People continue to be staying with bonds.

Another force at work is the aging of the baby-boomer generation.

As they approach retirement, People in america are shifting some of their opportunities away from stocks

to provide regular guaranteed income for the years when they’re no longer working.

And the flight from stocks may also be driven by households that are no longer able to tap into home equity for cash

and may simply need the money to pay for regular expenses.

Fidelity Investments recently documented that a record number of people required

so-called hardship withdrawals from their pension accounts in the second quarter.

These are early withdrawals intended to purchase needs like medical expenses.

According to the Investment Company Start, which surveys 4,Thousand households annually,

the appetite with regard to stock market risk among American investors of all ages

has been declining steadily since it peaked about 2001,

and the change is the majority of pronounced in the under-35 age group.

For a couple of months at the start of this year, things were looking up for stock market trading.

Optimistic about growth, investors were again putting their money into stocks.

In March and 04, when the stock market rose 8 percent,

$8.1 billion flowed into domestic stock shared funds.

But then came a grim reassessment of America’s economic potential customers

as unemployment remained stubbornly high

and personal sector job growth declined to take off.

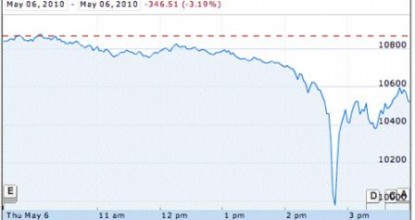

Investors’ nerves were additionally frayed by the “flash crash” upon May 6,

when the Dow jones Jones industrial index dropped 600 points in a matter of moments.

The authorities still do not know the reason why.

Investors pulled $19.1 billion from domestic equity funds within May,

the largest outflow because the height of the financial crisis in October 2008.

Over all, investors pulled $151.4 billion out of stock market mutual funds within 2008.

But at that time the market was tanking in shocking fashion.

The shock this time around is that Americans are withdrawing money

even when reveal prices are rallying.

The stock market rose Seven percent in July because corporate profits began rebounding,

but even that increase was not enough to tempt ordinary investors.

Instead, these people withdrew $14.67 billion from household stock market mutual funds in July,

according to the investment institute’utes estimates,

the third straight 30 days of withdrawals.

A big beneficiary has been bond funds, which offer regular fixed interest payments.

As traders pulled billions out of shares,

they plowed $185.31 billion into relationship mutual funds in the first seven months of this year,

and total bond fund opportunities for the year are on monitor to approach the record set in 2009.

Charles Biderman, chief executive associated with TrimTabs, a funds researcher, said

it wasn’t any wonder people were putting their money in bonds

given the depressing performance of equities over the past decade.

“People have lost lots of money over the last 10 years in the stock market,

while there has been a bull market in bonds,” he said.

“In the financial markets, there is one truism: flow follows performance.”

Ross Williams, 59, a residential area consultant from Grand Rapids, Minn.,

began to take profits from his stock funds when the market began to recover last year

and invested the money in short-term bonds,

afraid that shares would again drop, according to this article from the New York Occasions.

“We have a very volatile marketplace, so we should be in ties in case it goes down again,” he explained.

“If the market is moving up, I noticed we should be taking this money

and putting this into something more safe rather than leaving it at risk.”

David Caploe

Editor-in-Chief

EconomyWatch.com

President / acalaha.com