What more is there to say? Gold is money.

It always has been, and it usually will be.

The fact that gold is actually money is why central banks hate it so much.

Central banking institutions succeeded in creating national monopolies on currencies. Only the Bank of England can printing English bank notes. Only the US Federal Reserve can printing US dollar bills. Only the Reserve Bank of Australia can print Aussie dollars.

(Rare exceptions to this are Scottish and Northern Irish retail banks. They retain the right to print their own notes. However, there is an suggested backing from the Bank of England for these notes.)

However, even though central banks have succeeded in imposing legal tender laws, by outlawing just about all competing currencies, one thing is apparent.

As much as they may like to, main banks and governments cant abolish gold. They can try. The doyen from the progressive movement, the tyrant, Franklin Delano Roosevelt, signed an executive order in 1933 to confiscate privately held gold in america.

And Part IV of the 1959 Banking Act in Australia gives the governor general the power to demand the actual relinquishment of all private gold. Part IV is currently suspended, but the governor general could invoke this at any time.

Governments and central banking institutions may try to take private gold again. They detest gold because it gives individuals a way to protect against the wear and tear of paper money rising cost of living.

In todays Money Morning, my colleague, global strategist Jim Rickards, provides more background around the relationship between central banking institutions and gold, and where the actual gold price could mind next.

Read on below with regard to details

Cheers,

Kris

Gold the Once and Future Currency

Jim Rickards, Strategist, Strategic Intelligence

Is gold off the bottom?

Its unfortunate that markets are now decreased to reading Janet Yellens mind. But thats what happens after seven years of market intervention and central planning by the Federal Reserve.

Using my system, which combines complex dynamic systems analysis with unique access to relevant info, were able to draw some useful inferences about the future road to gold prices. Our estimation is that gold has now discovered a bottom and is ready to move steadily upward from current levels.

For those who are completely allocated in physical precious metal (I recommend about 10% of investible property), theres nothing more to do on that front. You can just sit tight and enjoy the ride.

For those who do not have the actual recommended allocation to physical gold, this is an attractive entry point and a chance to top up your allocation at the best prices in six years.

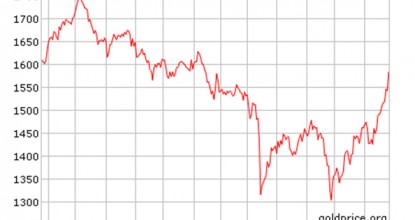

Its certainly already been a long and volatile ride for gold investors. Starting from a low of about US$250 per ounce in mid-1999, gold staged a spectacular rally of over 600% to about US$1,Nine hundred per ounce by July 2011. Unfortunately, that move looked increasingly unstable towards the end.

Gold was about US$1,400 for each ounce as late because January 2011. Almost US$500 for each ounce of the overall move occurred in just the last 7 months before the peak. That kind of hyperbolic growth is almost always nonsustainable.

Sure enough, gold fell dramatically from that peak to below US$1,100 per oz by July 2015. The 15-year chart still shows a gain of approximately 350%, but the four-year chart shows a loss of revenue of over 40%.

Those who invested during the 2011 rally are underwater, and many have given up on precious metal in disgust. For long time observers of gold markets, sentiment is the worst theyve seen.

|

Click to enlarge

Gold in dollars for each ounce, Sept. 2010-Sept. 2015

Source:?Wall Street Journal |

At?Strategic Intelligence, we glance behind the charts as well as sentiment and try to discern the actual systemic dynamics driving the price. Once those dynamics are specified, forecasting becomes much more reliable.

Weve identified three elements that well explain the gold price dynamics. These 3 factors are real interest rates, dollar strength and central bank intervention. Looking at the current status and likely path of these factors is the greatest guide to the future price of precious metal.

Real interest rates are one of the best predictors from the nominal dollar price of precious metal. When real interest rates are low (or negative), that provides gold a boost. When actual interest rates are high, which puts downward pressure upon gold.

The correlation is not perfect, but its much stronger than other correlations such as the stock market or economic growth. The reason for the actual correlation is easy to understand. Gold has no yield. Golds valuation needs to compete with other asset classes such as stocks and bonds that do possess yields. When yields upon competing asset classes are higher, the gold price tends to suffer, and?vice versa.

What matters for this function is not the?nominal?rate of interest however the?real?rate. Real rates of interest are defined as the nominal interest rate minus inflation. For instance, if the nominal interest rate is actually 5%, but inflation is 3%, then your real rate is only 2% (5% minus 3%). That sounds simple enough, but there are complications.

In selecting minimal interest rates, you have to specify the maturity. Rates on 2-year Treasury information are much lower than rates upon 10-year Treasury notes. We use the 10-year note rate for our analyses because its a good proxy for mortgage rates and corporate bond rates, which represent the cost of financing long-term investments in housing and fixed property by individuals and companies. It makes more sense to consider gold as a long-term core keeping than as a short-term trading instrument.

The other complication arises once the rate of inflation is larger than the nominal rate of interest. In that case, the real rate is negative. This might happen when the 10-year note rates are 1% and inflation is 2%.

In that position, the real rate is negative 1% (1% without 2%). That is the ideal environment for gold. A zero yield on gold is actually greater than the negative real deliver on notes.

Wall Street analysts keep talking about how low interest are. Its true that nominal minute rates are low, but real minute rates are quite high by historic standards. For the past several years, 10-year nominal rates have mostly been more than 2%, but inflation has been about 1%, sometimes lower.

This means that the real rate on 10-year notes has been over 1%. Compare this to the situation in 1980 (when gold strike a new high of $800 per oz). Back then, Treasury bonds yielded 13%, however inflation was 15%, so the real rate was?negative 2%.?Dont end up being misled by low minimal interest rates. Focus on the real prices instead and youll have better insight into the future price of precious metal.

The second factor is buck strength. There the relationship is even more striking. Should you consider gold to be a form of money or currency?(that we do? thats why we cover it in?Strategic Intelligence), then its easy to see that the strong dollar signals an inadequate dollar price of gold, along with a weak dollar signals a powerful dollar price of gold.

The greatest measure of dollar strength (apart from gold itself) is the Price-Adjusted Broad Dollar Index maintained through the Federal Reserve Board.

The all-time low for this dollar index was 80.5001 in July 2011, the time of which corresponds exactly using the all-time high dollar price for gold.

Conversely, that index today reads 95.595. Thats the highest studying in over six years. Not surprisingly, just as the dollar reaches a six-year high, gold is actually near a six-year low. Once again, the correlation is not ideal, but it is surprisingly robust.

Wall Street analysts have tended to select the wrong dollar indexes in performing their analysis.

The Wall Road indexes are heavily heavy toward the euro and yen, whereas the Feds catalog looks at emerging markets such as China. At?Strategic Intelligence, weve used the Fed index all along. A glance at Page 253 associated with my book?The Death associated with Money?confirms that weve always used the right index tool.

The 3rd factor is central financial institution intervention.

Here the case is straightforward: a simple matter of supply and demand. Mining result has been remarkably constant over recent decades: about 2,Thousand tons per year.

Gold has not many industrial uses.

I consider jewellery to be wearable wealth, so I do not distinguish between jewellery demand and bullion demand both are types of wealth preservation. So along with constant output and variable demand for gold as a shop of wealth, it has been relatively easy for central banks to control the price of gold by throwing gold reserves on the physical market at critical junctures.

There have been three major waves associated with central bank manipulation within the physical market.

The first had been the London Gold Swimming pool of the 1960s, which collapsed in 1968.

The second would be a covert effort by the U.S. and IMF to dump 1,700 tons of precious metal on the market from 1975C79 to conceal the real impact of rising cost of living. This collapsed in 1980 whenever both inflation and the cost of gold spun out of control.

The third effort was the Washington-inspired Central Financial institution Gold Agreement (CBGA), which formed the sellers cartel of 11 national central banks (not?including the Ough.S.).

The CBGA was created in 2000 and renewed in 2004 and 2009. The largest seller under CBGA was Switzerland. This particular agreement has now failed, and there have been no sales by any of the signatories since 2010.

Since after that, central banks have moved from being net sellers to net buyers the very first time in decades. With couple of official sellers and many recognized and nonofficial buyers, gold need now exceeds gold supply from mines, putting pressure on scrap gold and other fragile hands to fill the gap.

The importance?of this?analysis is that it doesnt focus on where we are. This focuses on where were going. Central banks cannot tolerate higher real interest rates, because they load consumption and investment.

The Federal Reserve cannot tolerate a strong buck because it imports deflation (in the form of lower import prices) from around the world. Physical financial markets are skewed toward excess need because China, Russia, Iran along with other countries continue to demand precious metal to diversify reserves away from dollars while output is flat and official product sales by the West have stopped.

All three factors real rates, the strong dollar and official sales are pointing towards a reversal of recent developments and momentum toward problems that favour higher gold costs.

Gold can move in either path, but it is much more likely to move upward than down given present conditions.

All the best,

Jim Rickards,

Strategist, Strategic Intelligence