TORONTO – Ontario Finance Minister Charles Sousa announced Thursday that the province’s budget deficit has shrunk a lot more than expected and that the Liberals take presctiption pace to return to a balanced budget by 2017-18, even as net debt is set to increase for the reason that timeframe.

Highlights from the 2016 Ontario budget

By Keith Leslie

Finance Minister Charles Sousa delivered the Ontario budget on Thursday. Here are a few from the highlights:

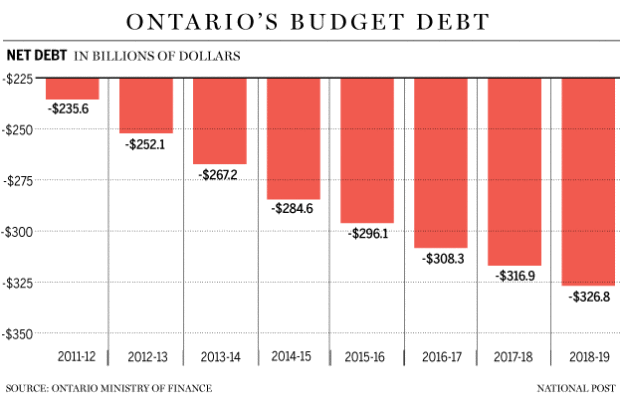

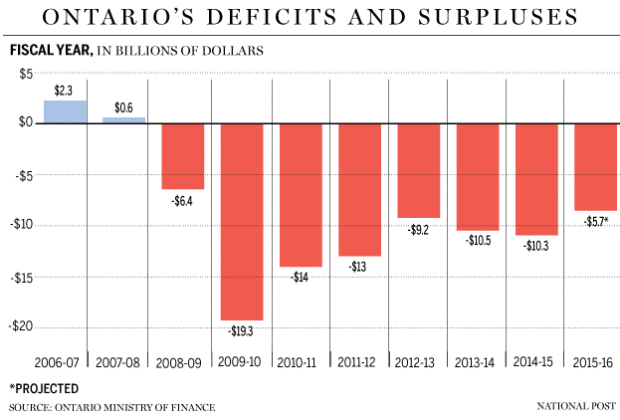

The budget deficit for fiscal year 2015-16 is anticipated in the future in at $5.7 billion, down in the last estimate of $7.5 billionThe deficit for 2016-17 is projected in the future in at $4.6 billion and become reduced to zero the following fiscal yearOntario’s net debt will hit $308 billion in 2016-17, the biggest of any sub-national jurisdiction in the world, costing $11.8 billion in interest payments, that will increase to $13.1 billion by 2018-19Income from the cap-and-trade intend to battle climate change is anticipated hitting $1.9 billion in 2017, up from last year’s projection of $1.3 billion

University and college tuition will be free for students from families with incomes of $50,000 or less, and most 1 / 2 of students from families with incomes up to $83,000 will get non-repayable grants that exceed the typical tuition – mostly students who survive their ownThere is a $3 increase in the cost of a carton of 200 cigarettes, effective at 12:01 a.m. Friday, and also the tobacco tax could keep rising at the rate of inflation each year within the next five years.The minimum price for a bottle of wine rises to $7.95, there is a number of increases in the LCBO’s mark-up on wine, starting with a two percentage point hike in June – about 10 cents a bottle – accompanied by another two percentage points in 2017 and 2018, with a one-point hike in 2019There may also be annual increases of about 10 cents within the tax on wine sold in private stores, increasing from 16.1 cents to 20.1 cents over four yearsThe $30 fee for Drive Clean vehicle emissions tests is going to be eliminated in 2017-18, although not the tests themselves, that will cost the province $60 million a yearHospitals can get their first funding rise in 5 years, up $345 million, plus $12 billion over Ten years in capital grants for around three dozen major hospital projectsSingle seniors earning as much as $19,300 each year is going to be eligible for cheaper drugs starting in August, compared with the prior threshold of $16,018. Couples by having an income of as much as $32,300 may also be eligible, where before only those earning $24,175 qualified. The costs will be offset by raising deductibles and co-payments for seniors above the new income thresholds. Annual deductibles will rise to $170 from $100 and co-payments will increase with a dollar to $7.11There will be $333 million over five years to revamp and improve autism servicesShingles vaccines for seniors, which cost $170, will be free.

The Canadian Press

Sousa asserted the deficit has become down in the $7.5 billion projected after this past year to $5.7 billion, as stronger economic growth in Ontario boosted government revenues. The budget forecasts that Ontario’s economy grew 2.5 percent in 2015, a significantly stronger level compared to 1.2 per cent forecast for the national economy.

Ontario’s deficit will also be helped by $1.1 billion gained from the sale of Hydro One, as well as growing cash injections in the authorities, that will hit $24.6-billion this year and rise to $26.6-billion by 2018.

But net debt goes up as the government continues to borrow to fund projects, including a massive $160 billion infrastructure project within the next 12 years. Net debt is set to increase to $326.8 billion in 2018-19, from $296.1 billion in 2015-16, even as the Liberals are set to possess a balanced budget by then.

The projection that Ontario’s debt will continue to rise and that debt-to-GDP will continue to hover near 40 per cent in the medium-term won’t thrill debt rating agencies. Standard & Poor’s downgraded the province’s debt last year, while others such as Moody’s Investors Service have placed an adverse outlook on provincial bonds.

Sousa dismissed the idea of further debt downgrades, however, saying a declining debt-to-GDP ratio could be welcomed.

“In my opinion credit agencies are going to look at this budget and understand that we’re achieving what we should said we’re going to do,” he said throughout a news conference.

The government has said it has a target of reducing net debt-to-GDP to the pre-recession degree of 27 per cent, although it gets no where near to that level in its projected forecast, with net debt-to-GDP hitting 38.5 in 2018-2019. The ratio is expected to peak at 39.6 per cent in 2015-16, remain level in 2016-17 and just begin to decline in 2017-18.

The government is projecting that total revenue in 2015-16 is going to be $2.2 billion greater than the 2015 budget had factored in, due to “higher asset optimization” and much more tax revenue as a result of a greater Ontario economy.

“I believe your budget is a huge part of the right direction,” said Douglas Porter, chief economist at BMO Capital Markets inside a phone interview. “The deficit targets were a substantial step away from the $10 billion deficits of past years.”

Patrick Brown, leader of Ontario’s Progressive Conservatives, said he cast doubt on the Liberals having the ability to go back to a balanced budget by its target date and warned that the budget was raising costs on Ontarians.

“The truth is taxes ‘re going up,” he explained.

Total government expenses within the upcoming fiscal year will be $0.2 billion higher than forecast within the 2015 budget. Program expenses is going to be $0.4 billion higher, but unchanged from the call produced in the 2015 Ontario Economic Outlook and Fiscal Review late last year. The increase in expenses is usually because of the Green Investment Fund, which includes a $325 million down payment aimed at reducing greenhouse gas emissions

The government is projecting a budget deficit of $4.3 billion in 2016-17, and balanced budgets in 2017-18 and 2018-19. The 2016-17 deficit projection is definitely an improvement of $0.5 billion when compared to forecast in the 2015 budget.

Related

- Ontario Budget 2016 walks tightrope between aspirations of social justice and hard fiscal realitiesOntario’s cap-and-trade program expected to raise $1.9B in newbie – but will not be used to lower deficitOntario might have surplus as high as $15B if spending have been restrained, Fraser Institute report saysOntario budget 2016’s free tuition pledge: What the changes mean for some students

The Liberal budget is obtaining a revenue boost from an Ontario economy that’s gaining steam. The province boasts one of the fastest growth rates in Canada, and Statistics Canada noted that 100,000 new jobs have been created there in the past Twelve months.

A weak loonie and low oil prices are helping manufacturers increase as exports become competitive again.

“They’re getting the aid of the subtle underlying improvement in the Ontario economy,” Porter said. “They’re also being helped by steady downdraft in low borrowing costs and debt service charges, which continue to flow to the main point here.”

“Spending restraint, unfortunately, was not just like advertised previously,” he added.

Real estate and construction continue being two biggest contributors to gross domestic product, though economists are increasingly worried about the red-hot Toronto housing industry, which is becoming a disproportionately large number of the economy.

Sousa noted that Ontario’s stronger economy is essential to balancing the budget.

“We have improved revenues from – the development in our economy and housing too,” he said.

And while debts are going up, the government said that it has reduced its risk to rate volatility by issuing long-term debt and locking in rates. The average rate of interest Ontario pays on its debt has declined from 10.9 per cent (on a weighted-average basis) to an expected 3.6 percent by March 31, 2015.

About $53 billion worth of bonds issued since the beginning of fiscal 2010-11 have been with terms longer than 30 years. The weighted-average term to maturity of long-term provincial debt issued has gone from 8.1 years in 2009-10, to 14 years in 2015-16.

Ontario is forecast to invest $11.2 billion servicing its debt in 2015-16, $210 million lower than forecast in the 2015 budget as a result of lower rates. But as debt rises, so will rate of interest payments, which are set to develop to $11.756 billion in 2016-17 and also to $12.453 billion in 2017-18.